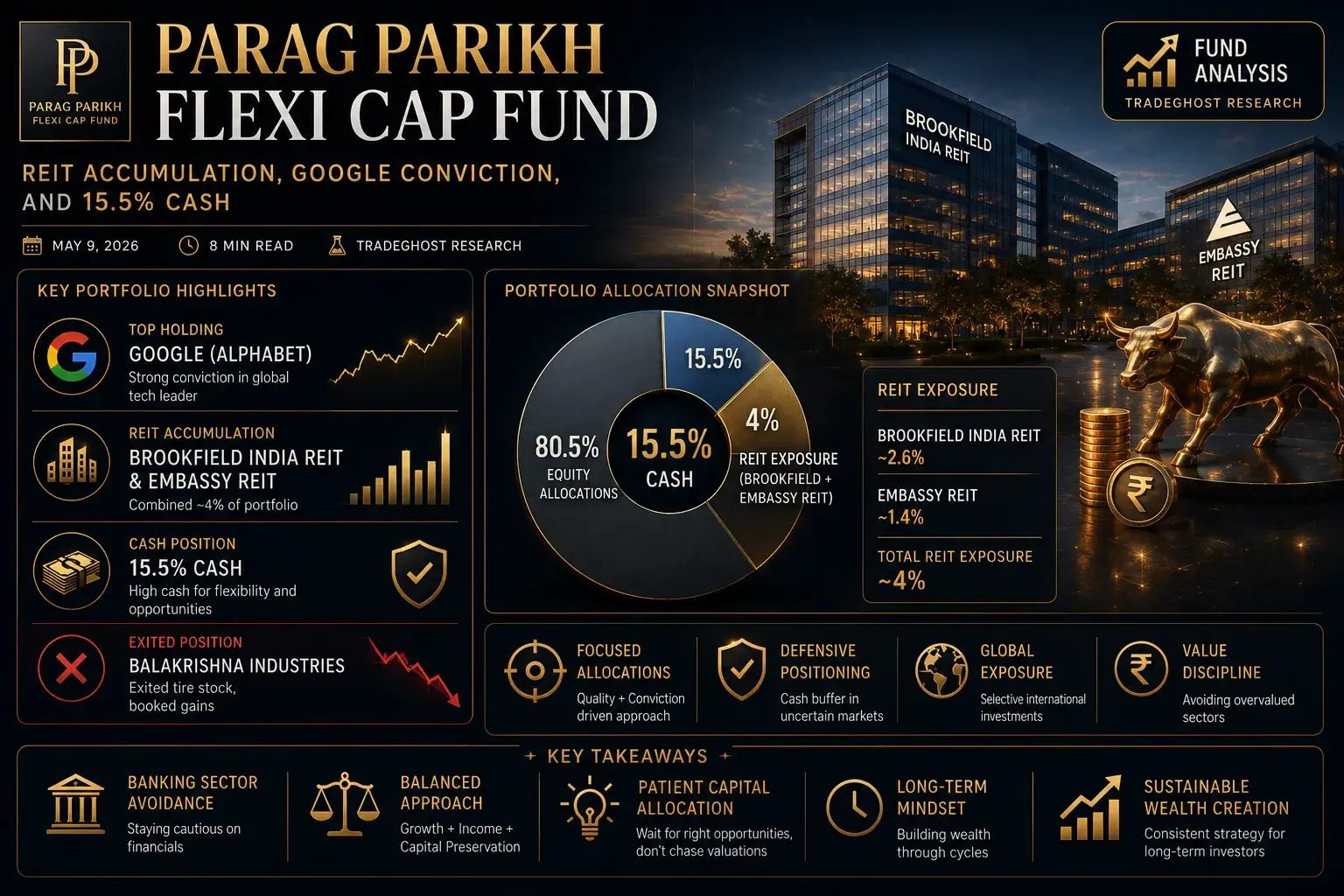

Parag Parikh Flexi Cap Fund's April portfolio activity reveals a manager increasingly convinced that Indian real estate investment trusts (REITs) offer the optimal risk-reward in a market where equity valuations have recovered and fixed-income yields remain unattractive. The fund significantly increased its allocation to Brookfield India REIT, building on earlier positions in Embassy REIT to create a concentrated REIT exposure that now represents approximately 4% of the total portfolio.

Significant additions to Brookfield India REIT, following earlier accumulation in Embassy REIT. Combined REIT exposure now approximately 4% of portfolio. The fund's top holding remains Google (Alphabet), reflecting the manager's comfort with global tech exposure even as domestic allocation shifts toward income-generating real assets.

Brookfield REIT: The New Conviction Bet

Brookfield India REIT offers exposure to Grade-A commercial office assets across India's top cities — a segment that has faced headwinds from work-from-home trends but is showing signs of stabilization as return-to-office mandates gain traction. The REIT's sponsor, Brookfield Asset Management, brings global institutional credibility and operational expertise that domestic developers struggle to match.

The fund's accumulation suggests the manager sees value in current REIT prices that discount overly pessimistic occupancy and rental growth assumptions. If office utilization recovers to 80%+ of pre-pandemic levels, Brookfield's portfolio should generate distribution yields of 7-8% with modest capital appreciation — an attractive proposition in a low-yield environment.

Google: The Anchor Position

Alphabet remains the fund's largest single holding, reflecting Parag Parikh's long-standing conviction in global technology leaders. Google's 40% price appreciation over the past month has amplified the position's portfolio impact, creating both performance contribution and concentration risk. The fund's discipline in holding through volatility — rather than trimming on strength — is consistent with its documented investment philosophy of letting winners run.

The Google position also serves a portfolio construction function: it provides USD-denominated exposure that acts as a natural hedge against rupee depreciation. With FII selling pressure continuing and the rupee under pressure, this global allocation has been particularly valuable for preserving purchasing power.

Balakrishna Industries Exit: The Tire Trade Concludes

The fund exited its position in Balakrishna Industries, a tire manufacturer that had been a portfolio holding for multiple quarters. The exit is notable because it contradicts the fund's typical buy-and-hold approach — suggesting either that the tire sector thesis played out fully, or that the manager identified superior opportunities elsewhere. Given the simultaneous REIT accumulation, the latter explanation seems more likely.

The tire sector has faced margin pressure from raw material costs (natural rubber, synthetic rubber, carbon black) and competitive intensity from both domestic and import competition. Exiting before these headwinds fully materialized demonstrates the fund's active risk management, even within its generally patient framework.

Banking Sector Avoidance: A Conscious Call

The transcript notes that the fund has avoided banking sector activity — a significant stance given that financials typically dominate Indian flexi-cap portfolios. This avoidance reflects either valuation discipline (banks have rallied significantly) or structural concerns (asset quality, NIM compression, regulatory risk). Given the fund's historical willingness to hold HDFC Bank and ICICI Bank through cycles, the current avoidance suggests specific concerns about the sector's risk-reward rather than a blanket financials aversion.

For investors in the fund, this underweight is a source of both relative risk and opportunity. If banks continue to outperform, the fund will lag peers. If banks face the margin and asset quality pressures that the manager appears to anticipate, the underweight will generate significant alpha.

Cash Position: Optionality at 15.5%

The fund's 15.5% cash position is elevated by historical standards and reflects the manager's difficulty in finding attractively priced opportunities in a market that has rallied 10-23% across segments. Rather than deploying cash into fully-valued positions, the fund is maintaining liquidity to capitalize on volatility — a patient approach that has historically served Parag Parikh investors well.

The cash also provides psychological comfort during drawdowns. Funds that are fully invested during corrections have no capacity to add to favored positions at distressed prices. Parag Parikh's cash buffer ensures that the next market dislocation will be met with buying power rather than forced selling.

Risk Factors

- REIT liquidity: Indian REITs are relatively illiquid; large position changes can move prices

- Concentration risk: Heavy Google exposure creates single-stock vulnerability

- Cash drag: 15.5% cash will underperform if markets continue rallying

- Style risk: The fund's value-oriented approach may lag in momentum-driven markets

Future Outlook

Parag Parikh Flexi Cap Fund's April activity reveals a manager navigating a challenging environment with characteristic discipline. The REIT accumulation, Google conviction, banking avoidance, and cash preservation all point to a portfolio positioned for volatility rather than momentum. This isn't a fund for investors seeking maximum near-term returns; it's a fund for investors seeking sustainable wealth preservation with selective growth exposure.

For existing investors, the current positioning should be viewed as defensive-aggressive — protecting capital while maintaining exposure to high-conviction ideas. For prospective investors, the fund's current cash level and valuation sensitivity suggest that a systematic entry (SIP) approach is preferable to lump-sum deployment.