Telangana is preparing a sweeping revision of government land values that will reshape real estate economics across the state — particularly in Western Hyderabad, where market transaction prices have long diverged from official valuations. The proposed revision, expected by end of May 2026, will increase government land rates by 20% to 100% across all districts, with the sharpest increases concentrated in high-demand corridors where current market rates vastly exceed official benchmarks.

Government land values to be revised upward by 20-100% across Telangana, effective end of May 2026. The revision targets agricultural land where government values (₹70,000 per acre in some areas) lag market transaction prices (₹40-50 lakh per acre) by orders of magnitude. Registration charges and stamp duty will rise proportionally, generating an estimated ₹4,000 crore in additional government revenue.

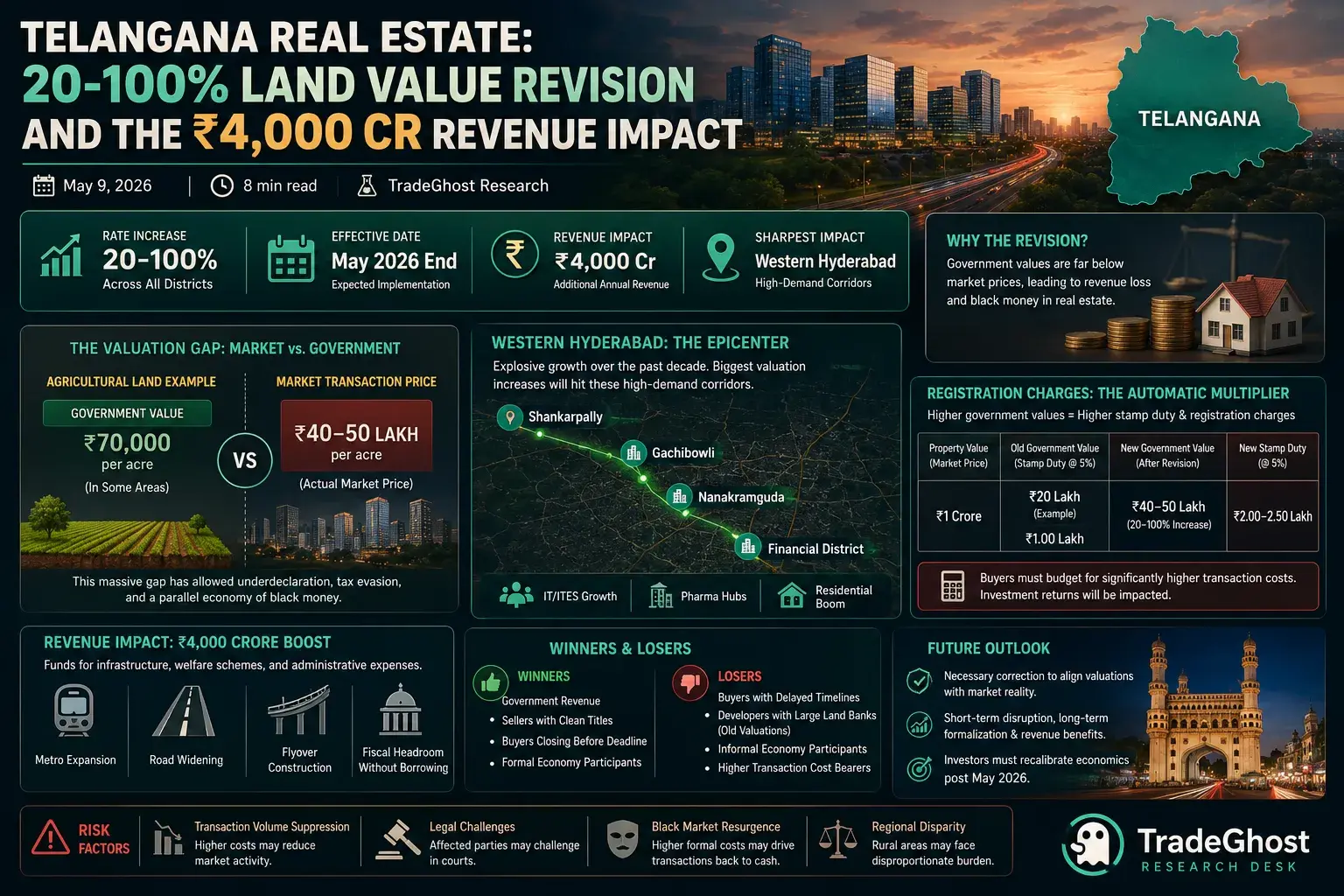

The Valuation Gap: Market vs. Government

India's real estate market operates on a dual-track pricing system: market values reflect actual transaction prices, while government values serve as the base for stamp duty, registration charges, and capital gains calculations. In Telangana, this gap has become absurd — agricultural land trading at ₹40-50 lakh per acre carries a government value of merely ₹70,000 per acre, or sometimes just a few lakh rupees.

This divergence isn't accidental; it's a feature of India's property tax system that has historically allowed buyers and sellers to underdeclare transaction values, reducing tax burdens while creating a parallel economy of black money. The government's revision is an attempt to narrow this gap, capture legitimate revenue, and bring more transactions into the formal financial system.

Western Hyderabad: The Epicenter

Western Hyderabad — encompassing Gachibowli, Financial District, Nanakramguda, and the emerging corridors toward Shankarpally — will see the sharpest valuation increases. This region has experienced explosive growth over the past decade, driven by IT/ITES expansion, pharmaceutical clusters, and residential development. Market land prices have appreciated 5-10x, while government values remained frozen at decade-old levels.

The revision will have immediate transaction consequences. Buyers who were planning purchases in June 2026 are now rushing to complete deals before the new rates take effect, creating a temporary surge in registration activity. Sellers, conversely, may delay transactions to benefit from higher benchmark values for capital gains calculations. The net effect on transaction volumes is uncertain but likely to be disruptive in the short term.

Registration Charges: The Automatic Multiplier

Because registration charges and stamp duty are calculated as percentages of government value (not market value), the valuation revision automatically increases transaction costs. A property that previously attracted ₹2 lakh in stamp duty may now attract ₹4-5 lakh — a significant additional outlay that buyers must budget for.

For investors, this cost increase changes the economics of real estate investment. Yield calculations must now incorporate higher entry costs, and exit calculations must account for higher transfer expenses. The revision effectively reduces the net return on real estate investments, potentially redirecting some capital toward alternative asset classes.

Revenue Implications: ₹4,000 Crore Boost

The government expects ₹4,000 crore in additional annual revenue from the revision — a substantial sum that will fund infrastructure, welfare schemes, and administrative expenses. For a state that has been aggressive in capital expenditure (Hyderabad's metro expansion, road widening, flyover construction), the revenue boost provides fiscal headroom without additional borrowing.

The revenue estimate assumes transaction volumes remain stable post-revision. If higher costs suppress activity, the actual collection may fall short. Historical experience from other states (Andhra Pradesh's 2019 revision, Karnataka's periodic updates) suggests an initial volume dip followed by normalization as market participants adjust to the new cost structure.

Market Impact: Winners and Losers

The revision creates clear winners and losers. Government revenue wins. Sellers with clean titles win (higher benchmark values reduce capital gains tax incidence). Buyers with urgent timelines win (if they complete before the deadline). Losers include: buyers with delayed timelines facing higher costs; developers with large land banks valued at old rates; and the informal economy participants who relied on underdeclaration for tax avoidance.

For listed real estate developers with Telangana exposure (Aparna, My Home, Lanco, Ramky), the impact is mixed. Existing inventory benefits from higher replacement costs (supporting pricing power), but new land acquisitions face higher entry costs. The net effect depends on each developer's land bank vintage and acquisition strategy.

Risk Factors

- Transaction volume suppression: Higher costs may reduce market activity, offsetting rate increases

- Legal challenges: Affected parties may challenge the revision in courts, creating uncertainty

- Black market resurgence: Higher formal costs may drive transactions back to cash-based underdeclaration

- Regional disparity: Rural areas with lower appreciation may face disproportionate burden

Future Outlook

Telangana's land value revision is a necessary correction to a system that had become divorced from market reality. The short-term disruption will be significant, particularly in Western Hyderabad where transaction costs could increase 50-100%. But the long-term benefits — formalization, revenue generation, and reduced black money — justify the transition pain.

For real estate investors, the revision reinforces the importance of timing and location. Pre-revision transactions in high-appreciation corridors offer cost advantages that will disappear after May 2026. Post-revision, investment economics must be recalibrated to reflect the new cost structure. The fundamental demand drivers (IT growth, infrastructure expansion, urbanization) remain intact; only the transaction cost mathematics has changed.