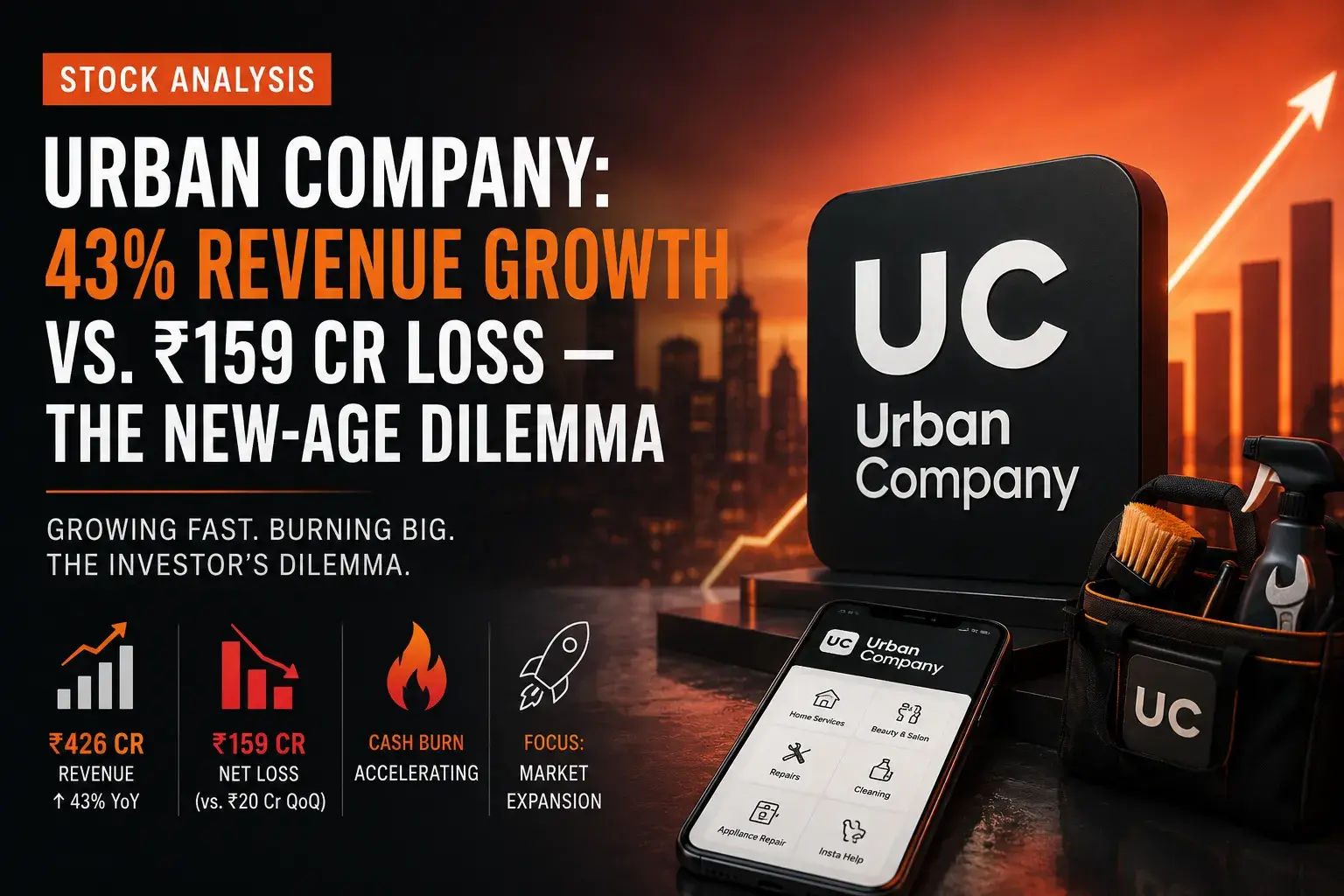

Urban Company's quarterly results present a stark dichotomy that defines the new-age tech investment dilemma: a business successfully scaling revenue while burning cash at a rate that challenges the patience of even the most growth-oriented investors. Revenue climbed 43% year-on-year to ₹426 crore, but losses ballooned to ₹159 crore — a dramatic deterioration from the ₹20 crore loss posted in the previous quarter.

From ₹20 crore loss to ₹159 crore loss in a single quarter — this isn't a gradual path to profitability. CEO Abhiraj Bansal explicitly stated that losses will continue to grow in coming quarters as the company prioritizes market expansion over near-term margins. For investors expecting a quick turnaround, this guidance is sobering.

Revenue Growth: Genuine but Expensive

The 43% revenue growth is undeniably impressive in a consumer environment that's been uneven at best. Urban Company's home services marketplace — spanning beauty, cleaning, repairs, and wellness — is capturing genuine demand as India's urban middle class increasingly outsources domestic tasks. The Insta Help business, in particular, has gained strong traction as a quick-commerce adjacent service.

However, the cost of this growth is becoming prohibitive. Customer acquisition costs in the home services space are notoriously high due to low purchase frequency and high service variability. Unlike food delivery or ride-hailing, where daily usage creates natural habits, home services are episodic — making loyalty programs and subscription models less effective at reducing CAC.

Insta Help: The Bright Spot with a Dark Side

Insta Help, Urban Company's quick-response service vertical, has achieved the product-market fit that eludes many new-age startups. The service is gaining consumer mindshare and generating repeat usage. But here's the critical issue: Insta Help's success is directly correlated with the company's cash burn. Each new city launch, each marketing push, each partner incentive program consumes capital that isn't being replenished by operational cash flow.

Management's commentary was unapologetic about this trade-off. The explicit message: growth now, profits later. This isn't a unique stance in the startup ecosystem, but it requires investors to have conviction about the company's ability to eventually monetize its installed base. The question isn't whether Urban Company can grow; it's whether the eventual profits will justify the cumulative losses.

Unit Economics: The Unanswered Question

The quarterly disclosure didn't provide granular unit economics — contribution margins per service category, payback periods on customer acquisition, or partner retention rates. This opacity is frustrating for fundamental investors who want to model path-to-profitability scenarios. What we know is that the aggregate economics are negative and trending worse. What we don't know is whether specific categories or geographies are already profitable and cross-subsidizing the expansion.

For a company that's been public for multiple quarters, the lack of detailed unit economics disclosure is a red flag. It suggests either that the numbers aren't flattering enough to share, or that management doesn't believe investors are sophisticated enough to parse them. Neither interpretation is encouraging.

Competitive Landscape: Defensible but Not Impenetrable

Urban Company's first-mover advantage in organized home services is real. The brand recognition, partner network, and operational infrastructure create switching costs for both service providers and consumers. However, the barriers to entry aren't insurmountable. Local competitors, vertical specialists, and even quick-commerce players expanding into adjacent services all represent competitive threats.

The moat is wider than in ride-hailing (where switching between Uber and Ola is frictionless) but narrower than in food delivery (where network effects are stronger). Urban Company's competitive position is best described as "defensible but requiring constant investment" — which explains the persistent cash burn.

Technical Outlook: Distribution Pattern

The stock has been in a distribution phase since its IPO pop, with each rally meeting aggressive selling. The earnings reaction was predictably negative, with the stock breaking toward lower support levels. For technical traders, this is a stock to avoid on the long side until a clear accumulation pattern emerges.

Support levels are difficult to identify because the stock lacks sufficient trading history to establish reliable technical references. The IPO price provides a psychological anchor, but in the current environment, psychological support often fails when fundamental narratives deteriorate.

Risk Factors

- Funding runway: At current burn rates, the company may need to raise capital within 12-18 months, potentially at depressed valuations

- Profitability timeline: Management's guidance suggests no near-term path to breakeven, testing investor patience

- Partner churn: Service professional retention is critical; any deterioration would directly impact service quality and customer retention

- Macro sensitivity: Home services are discretionary; economic slowdowns could compress demand faster than the company can reduce fixed costs

Future Outlook

Urban Company is a bet on India's service economy formalization — a megatrend that is undeniably real but whose timing and profitability remain uncertain. The company has built a genuine platform with real consumer traction. What it hasn't built is a credible path to profitability that doesn't require years of additional capital consumption.

For venture capital and growth equity investors, this profile is acceptable. For public market investors seeking near-term returns, it's problematic. The stock is appropriate only for portfolios with long time horizons, high risk tolerance, and conviction about India's digital services transformation. Everyone else should wait for either a dramatic valuation reset or tangible evidence of unit economics improvement.